Sign in

Request a demo

Talk with an accountant.

Connect with us:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Get a clear, practical breakdown of the ASC 606 five steps. Learn how to apply each step for accurate revenue recognition and confident financial reporting.

As your business grows, so does the complexity of your financial reporting. What worked with a handful of customers can become unmanageable when you’re dealing with hundreds or thousands of transactions. This is where the ASC 606 standard becomes so critical. It provides a scalable framework that ensures your revenue recognition practices can keep pace with your success. The standard is built around a core methodology called the ASC 606 five steps, which provides a consistent process for every customer contract. Mastering this model is essential for any company aiming for sustainable growth, as it creates the solid financial foundation needed to pass audits and make data-driven decisions with confidence.

If you’ve ever felt like financial regulations were written in another language, you’re not alone. But ASC 606 is one standard you’ll want to get familiar with. Think of it this way: ASC 606 is a common set of rules for all businesses to follow when counting money earned from customer sales. It was created to make revenue reporting consistent across different industries, so everyone is playing by the same rulebook.

Why does this matter for you? Getting revenue recognition right isn't just about staying compliant. It gives you a true, accurate picture of your company’s financial health. This clarity is essential for making smart strategic decisions, passing audits with confidence, and showing potential investors that your business is on solid ground. With the right systems in place, you can turn complex compliance requirements into a powerful tool for growth.

Before ASC 606, different industries had their own ways of reporting revenue. This made it incredibly difficult to compare the financial performance of, say, a software company and a construction firm. The standard simplifies this by creating one core principle for everyone. The main idea is to recognize revenue when a company delivers its promised goods or services to customers, for the amount the company expects to receive in return. This shifts the focus from when you get paid to when you actually earn the money, providing a more accurate reflection of your business operations.

Technically, public companies and large private businesses (those with over $25 million in annual revenue) are required to follow ASC 606. However, its reach extends much further. Startups often need to be compliant to get money from investors or secure bank loans, as financiers want to see standardized, reliable financial statements. The reality is that all companies, both public and private, should understand and apply these rules, especially as their business models evolve. Adopting this standard early on prevents major headaches down the road and sets your business up for scalable, profitable growth.

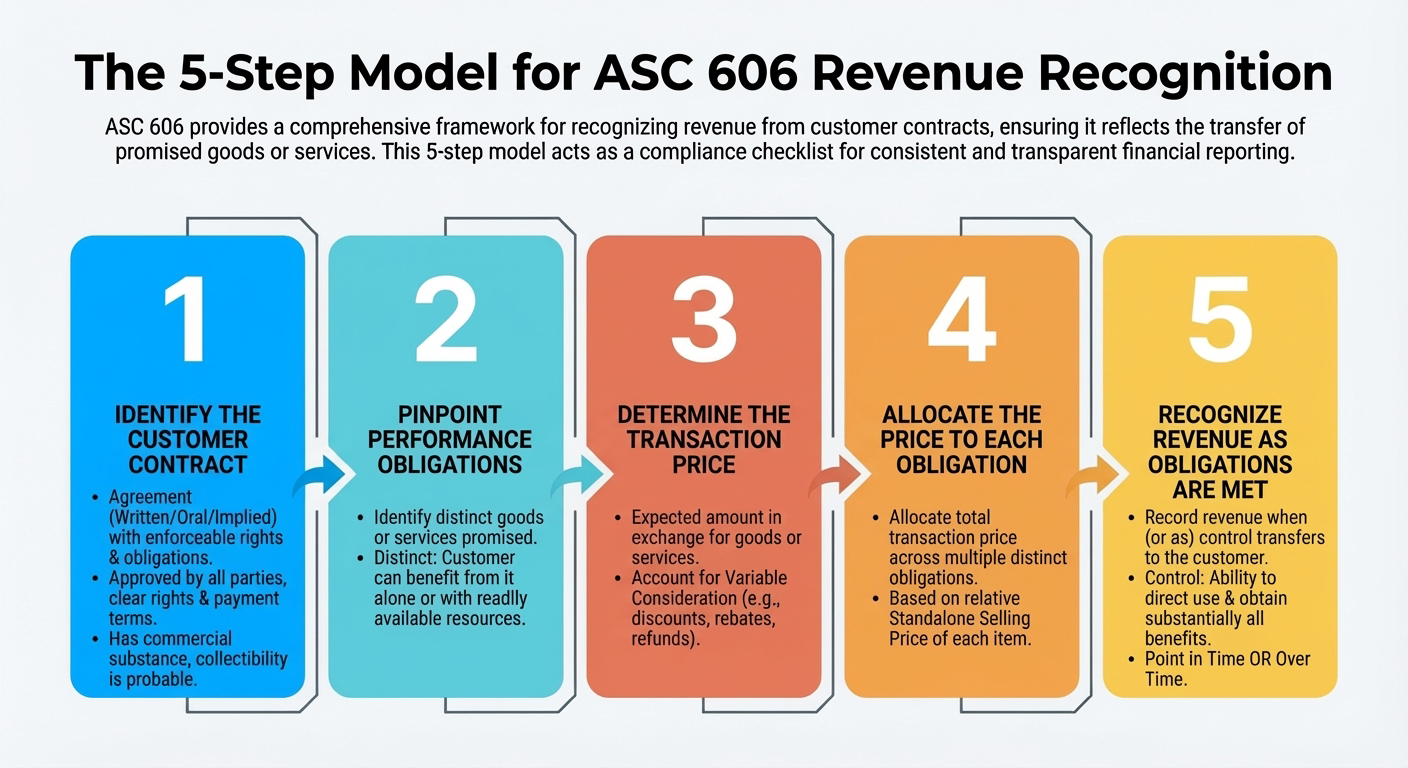

At its core, ASC 606 provides a single, comprehensive framework for recognizing revenue from customer contracts. This framework is built around a five-step model that guides you through the entire process, from the initial agreement to the final entry in your ledger. The goal is to ensure that you recognize revenue in a way that accurately reflects the transfer of promised goods or services to your customers.

Think of these five steps as a checklist for compliance. By working through them for each customer contract, you create a consistent and transparent process for your financial reporting. This not only helps you meet regulatory requirements but also gives you a clearer picture of your company's financial performance. Whether you're dealing with a simple one-time sale or a complex, multi-year subscription, this model is your roadmap. Let's break down what each step involves.

First things first, you need to confirm you have a contract with a customer. Under ASC 606, a contract is any agreement between two or more parties that creates enforceable rights and obligations. This doesn't always mean a lengthy document filled with legal jargon and signatures. A contract can be written, oral, or even implied by your standard business practices. For an agreement to qualify, it must meet a few key criteria: both parties have approved it, the rights and payment terms for goods or services are clear, it has commercial substance, and you are likely to collect the payment you're entitled to.

Once you have a contract, the next step is to identify your specific promises to the customer. These promises are called "performance obligations." A performance obligation is a promise to transfer a distinct good or service. The key word here is distinct. A good or service is considered distinct if the customer can benefit from it on its own or with other readily available resources. For example, if you sell a software subscription along with a separate, optional training package, you likely have two separate performance obligations because the customer can use the software without the training.

Now it's time to figure out how much you'll get paid. The transaction price is the amount of money you expect to receive in exchange for transferring your goods or services. This might sound straightforward, but it can get complicated. The price isn't always a fixed number. You need to account for any "variable consideration," which includes things like discounts, rebates, refunds, credits, or performance bonuses. Accurately estimating these variables is a critical part of determining the final transaction price and is a common challenge for many businesses.

If your contract has multiple performance obligations (as identified in Step 2), you can't just recognize the total contract value in one lump sum. Instead, you need to allocate the total transaction price across each separate obligation. This allocation is based on the relative standalone selling price of each distinct good or service. The standalone selling price is simply the price you would charge a customer for that item if you sold it separately. This step ensures that you assign a fair value to each promise you've made to the customer.

This is the final and most important step: actually recording the revenue. You can recognize revenue only when (or as) you satisfy a performance obligation by transferring control of a good or service to the customer. "Control" means the customer has the ability to direct the use of and obtain substantially all of the remaining benefits from the asset. This transfer can happen at a single point in time (like when a customer buys a coffee) or over time (like with a year-long consulting engagement). Automated revenue recognition solutions can help ensure accuracy here, especially for high-volume businesses.

Once you have a contract, the next step is to figure out exactly what you’ve promised to deliver. In ASC 606 terms, these promises are called “performance obligations.” It sounds technical, but it’s really just a list of the specific goods or services you owe the customer. This could be a single item, like a software license, or a bundle of things, like a new phone, a setup service, and a monthly data plan.

The main goal here is to break down the contract into its individual components. Why? Because you can only recognize revenue when you’ve fulfilled a specific promise. If your contract includes multiple obligations, you’ll likely recognize revenue at different times for each one. For example, you’d recognize revenue for a product when it’s delivered, but you’d recognize revenue for a related service over the time you provide it. Getting this step right is crucial for accurate timing, and it’s where having clear data visibility into your sales and service agreements becomes incredibly important.

For a promise to be considered a separate performance obligation, it needs to be “distinct.” This is a key concept in ASC 606. According to the standard, a good or service is distinct if two conditions are met. First, the customer can benefit from it on its own or with other resources they already have. Think of it this way: could you sell this item separately? For example, a one-time installation fee for a new software system is distinct because the customer gets a clear benefit from the setup itself. Second, the promise to transfer the good or service is separately identifiable from other promises in the contract.

Many contracts bundle multiple goods and services together. Your job is to look at that bundle and identify each distinct promise. A classic example is a telecom contract that includes a new phone and a two-year service plan. The phone is one performance obligation, and the monthly service is another. They are sold together, but they are distinct promises. The customer can use the phone with another carrier, and the service can be used on another phone. Separating these obligations ensures you recognize the revenue for the phone upfront and the revenue for the service over the two-year contract term.

Another critical question to ask is whether you are acting as a principal or an agent. This determines how much revenue you get to record. If you control the good or service before it’s transferred to the customer, you’re the principal. In this case, you record the gross amount of the sale as revenue. However, if you are simply arranging for another party to provide the good or service, you’re an agent. As an agent, you only record your fee or commission as revenue. This distinction is vital for marketplaces and resellers, and it’s an area where having an automated system can prevent major accounting errors. If you're unsure how this applies to your business, it might be a good time to schedule a consultation.

Once you’ve identified your performance obligations, it’s time to attach a dollar amount to them. This covers steps three and four of the ASC 606 model: determining the transaction price and then allocating it across your obligations. This isn't always as simple as looking at the price tag, especially when contracts include variables or bundled services. Getting this right is fundamental to recognizing revenue accurately and requires a consistent method for assigning value to each promise you’ve made to your customer.

Many contracts aren’t for a single, fixed price. The final amount might change based on discounts, refunds, or performance bonuses. This is called "variable consideration." Under ASC 606, you can't just wait and see; you must estimate the amount you expect to receive and include it in the transaction price from the start. This means using historical data to make a reasonable forecast. For high-volume businesses, tracking these variables manually is nearly impossible, which is why real-time data visibility is so important for accuracy.

When you sell multiple products or services together for one price, you need to allocate that price to each item. To do this, you determine the standalone selling price (SSP) for each one. The standalone selling price is what you would charge a customer for that item if they bought it separately. If you don't have an observable SSP, you'll need to estimate it using a consistent method, like a market assessment or cost-plus-margin approach. This ensures the price is allocated proportionally based on value.

Contracts often change. A customer might add services, change the scope, or renegotiate pricing. When a contract is modified, you have to assess whether the change creates a new contract or alters the existing one. This decision impacts how you recognize revenue going forward. For example, adding a distinct new service at its standalone price is typically treated as a new contract. Managing these modifications correctly requires a system that can handle complexity and has effective integrations with your other financial tools.

Following the five-step model for ASC 606 isn't always a simple matter of checking boxes. The standard requires you to make significant judgments and estimates, especially when your contracts are complex. This is where many companies feel the strain, as these decisions directly impact how and when revenue appears on the books. Getting them right is essential for accurate financial reporting and for passing an audit with confidence.

Making these calls consistently and defensibly is much easier when you have solid data to back you up. You’ll need to look at historical trends, contract specifics, and customer behavior to inform your choices. This is where having a centralized system that provides clear data visibility becomes invaluable. It helps you move from guesswork to data-driven decisions, ensuring your approach is sound and repeatable across all your customer agreements. These judgments are a core part of the compliance process, and they fall into a few key areas.

One of the most important judgments you'll make is determining if your company is acting as a principal or an agent. This decision comes down to control. Are you the one directly providing the promised goods or services to the customer? If so, you’re the principal and you’ll record the full (gross) amount of the sale as revenue.

If you’re simply arranging for another party to provide the goods or services, you’re an agent. In this case, you only record the net amount you expect to keep—your fee or commission. This distinction can dramatically change your top-line revenue figures, so it’s a critical call to make for every transaction where other parties are involved.

Many contracts aren't for a single, fixed price. They often include variable consideration—things like discounts, rebates, credits, performance bonuses, or penalties. ASC 606 requires you to estimate these variable amounts and include them in the transaction price from the start.

The catch is that you can only include an amount if it's "highly probable" that you won't have to reverse it later. This means you need a reliable method for forecasting outcomes based on your historical data and contract terms. You also have to decide if a variable amount applies to the entire contract or just one specific performance obligation, which adds another layer to the estimation process.

As you review a contract, you need to identify each specific promise you’ve made to the customer. The challenge is figuring out which of these promises are "distinct" performance obligations. A good or service is considered distinct if the customer can benefit from it on its own and if your promise to deliver it is separate from your other promises.

For example, is the implementation service you offer with your software a distinct obligation, or is it integral to the software itself? Answering this requires judgment. This assessment is fundamental to the entire process, as it dictates how you’ll ultimately allocate the transaction price and recognize revenue over time.

Getting a handle on the five-step model is one thing, but putting it into practice is where things can get complicated. Many businesses, especially those with high-volume transactions or complex contracts, run into the same set of challenges when they start implementing ASC 606. The good news is that these hurdles are well-documented, and understanding them is the first step to building a process that works.

From figuring out exactly when you can count your money to untangling bundled services, these common issues often require careful judgment and a hard look at your existing systems. Let’s walk through the three biggest challenges you’re likely to face and how to think through them.

One of the biggest mental shifts with ASC 606 is its focus on when control of a good or service is transferred to the customer. It requires you to recognize revenue as you satisfy your performance obligations, not necessarily when you send an invoice or when cash hits your bank account. This can feel counterintuitive if you’re used to older, simpler methods.

For example, if a customer pays for a year-long software subscription upfront, you can't recognize that full amount in the first month. Instead, you have to recognize one-twelfth of the revenue each month as you deliver the service. This change aligns revenue with value delivery but can significantly impact your financial statements and requires a more sophisticated way of tracking revenue over time.

If your business offers multiple products or services in a single contract, you’ll need to spend some time on Step 2: identifying performance obligations. The standard requires you to determine if each promised good or service is “distinct,” meaning the customer can benefit from it on its own. This is where a lot of judgment comes into play.

Is your software license a separate item from the installation and training services you also provide? Or are they all part of one combined solution? Answering this correctly is critical because it dictates how you allocate the transaction price. Misinterpreting these obligations can lead to inaccurate revenue reporting and compliance issues down the road. This is especially tricky for SaaS, telecommunications, and other industries with bundled offerings.

ASC 606 isn’t just an accounting problem; it’s a business-wide operational challenge. The standard impacts everything from how your sales team structures contracts to the data your IT systems need to track. Many legacy accounting systems and spreadsheets simply aren't built to handle the complexities of allocating revenue across multiple obligations and recognizing it over different time periods.

This often means you need to update your tools and workflows to ensure compliance. Your systems must be able to manage contracts, track performance obligations, and handle variable pricing automatically. Without the right infrastructure, you risk manual errors, time-consuming reconciliations, and a lack of visibility into your true financial performance. Ensuring your tools have seamless integrations with HubiFi can help bridge these gaps and automate the process.

Adopting ASC 606 is more than just a change in accounting rules; it fundamentally reshapes how you present your company's financial story. This standard impacts everything from the numbers on your income statement to the footnotes that explain them. It requires a deeper look at your contracts, a more disciplined approach to your internal processes, and a greater level of transparency in your reporting. Getting it right means your financial statements will offer a clearer, more accurate picture of your revenue streams. But it also means you’ll likely need to adjust your systems, retrain your team, and rethink how you document every transaction. Let's walk through the key areas where you'll feel the effects.

Under ASC 606, you can't just report a top-line revenue number and call it a day. The standard requires much more detailed disclosures to give investors and other stakeholders a complete view. You’ll need to clearly explain the nature, amount, timing, and any uncertainty related to your revenue and cash flows from customer contracts. Think of it as telling the story behind the numbers. This includes breaking down revenue by category, providing details on your performance obligations, and explaining the significant judgments you made in the process. The goal is total transparency, ensuring anyone reading your financial statements understands exactly how your company makes money.

Implementing ASC 606 will likely put your existing systems and processes to the test. The new framework touches everything from financial reporting and internal controls to the very language in your customer contracts. You need to have solid processes in place to ensure revenue is recognized accurately and consistently. This means documenting every step of the five-step model for each contract, from identifying performance obligations to allocating the transaction price. Every estimate and judgment call must be supported by clear, logical documentation. Without it, you’ll face a tough time during audits and risk non-compliance.

A smooth transition to ASC 606 starts with a plan. First, conduct a gap analysis to see how your current revenue recognition practices stack up against the new standard. You'll need to establish clear processes for reviewing revenue estimates, especially when dealing with variable consideration. This isn't a one-time fix; it requires ongoing diligence. Your technology stack is another critical piece of the puzzle. Ensure your ERP and accounting systems can handle the new requirements. For many businesses, this means adopting automated solutions that offer seamless integrations with your existing tools to manage data and streamline compliance. Getting your systems, policies, and team aligned will make audits much more comfortable.

Implementing ASC 606 can feel like a huge project, but you don’t have to go it alone. Having the right tools and a solid plan makes all the difference. It’s about working smarter, not harder, to get your revenue recognition process on track and keep it there. Think of it as building a support system for your financial operations. With a combination of smart technology, team education, and consistent oversight, you can handle the transition smoothly and confidently. Let's walk through the key resources that will help you succeed.

Manual spreadsheets are a recipe for trouble when it comes to ASC 606. They’re prone to human error, difficult to scale, and can quickly become a compliance nightmare. An automated solution is the best way to manage revenue recognition accurately. These systems are designed to handle the complexities of the five-step model, from allocating transaction prices to recognizing revenue at the right time. Platforms like HubiFi streamline the entire process, ensuring you stay compliant without the manual headaches. By connecting directly with your existing tools, our solution offers seamless integrations that pull all your revenue data into one place, giving you a clear and accurate picture of your financials.

ASC 606 impacts more than just your accounting department. It can change how your sales team structures deals, how your legal team writes contracts, and how you report financial performance. Because these changes ripple across the company, it's essential to get everyone on the same page. Training is key to a smooth transition. Your team needs to understand the new framework and how it affects their specific roles, from financial reporting to internal controls. Think of it as a company-wide alignment that ensures everyone is speaking the same language when it comes to revenue. For more deep dives into financial operations, you can always explore our insights.

Getting compliant with ASC 606 is the first step, but staying compliant is an ongoing process. The standard requires you to provide clear and detailed information in your financial reports so that stakeholders can understand the timing, amount, and nature of your revenue. This means you need a system for continuous monitoring. Regularly reviewing your contracts and financial data helps you catch any discrepancies and adapt to changes in your business. An automated platform is invaluable here, as it provides the real-time analytics needed for effective oversight. If you’d like to see how automation can simplify ongoing compliance, feel free to schedule a demo with us.

Getting your revenue recognition process aligned with ASC 606 is a huge accomplishment, but the work doesn’t stop there. Staying compliant is an ongoing effort that requires diligence and the right systems. Think of it less like a project with a finish line and more like a routine practice that keeps your financial reporting healthy and accurate. When you treat compliance as a continuous process, you protect your business from costly errors and ensure your financial statements are always a reliable source of truth for investors, auditors, and your own leadership team. This isn't just about checking a box for the auditors; it's about building a resilient financial foundation that supports smart, strategic decisions as your company grows.

Building a sustainable compliance strategy comes down to a few core habits. It’s about creating clear documentation, consistently reviewing your customer agreements, and using technology to connect the dots. By embedding these practices into your operations, you can move from simply meeting the standard to using it as a tool for clearer financial insight. Let’s walk through three essential practices that will help you maintain ASC 606 compliance with confidence and turn a complex requirement into a competitive advantage.

One of the most important aspects of ASC 606 is transparency. It’s not enough to just report the final revenue numbers; you have to show your work. A clear audit trail provides a detailed record of the judgments, estimates, and methodologies you used to recognize revenue. This documentation should explain the nature, amount, and timing of your revenue streams, giving auditors and stakeholders a complete picture. Think of it as the story behind your numbers. Keeping meticulous records of every decision ensures that when questions arise, you have the answers ready. This practice is fundamental to building trust and passing audits without a hitch.

Your customer contracts are the foundation of revenue recognition, and they aren't static. As your business evolves, so will your agreements. That’s why a one-time review isn’t sufficient. You need a systematic process for reviewing all new and modified contracts to identify performance obligations and any changes that might affect revenue timing. Management must carefully determine when control of a good or service has passed to the customer. A regular review cadence ensures you consistently apply the five-step model correctly, even as your deals become more complex. This proactive approach helps you catch potential issues before they impact your financial statements.

Relying on spreadsheets and manual data entry to manage ASC 606 is a recipe for errors and wasted time. The standard is complex, and manual processes simply can’t keep up with high-volume transactions or intricate contracts. An automated revenue recognition solution is the most effective way to ensure accuracy and efficiency. By creating seamless integrations between your systems—like your CRM, ERP, and billing platforms—you create a single source of truth for all revenue-related data. This not only reduces the risk of human error but also automatically generates the detailed documentation needed for a clean audit trail, freeing up your team to focus on more strategic work.

Does my small business really need to worry about ASC 606? While the official mandate applies to larger public and private companies, all businesses should pay attention to ASC 606. If you ever plan to seek investment, apply for a loan, or sell your company, you’ll need financial statements that follow these rules. Adopting the standard early on builds a strong financial foundation and prevents a massive cleanup project down the road. It’s much easier to start with good habits than to fix bad ones later.

What's the difference between recognizing revenue 'over time' and 'at a point in time'? Think of it this way: revenue is recognized when your customer gets control of what they paid for. If that happens all at once, it’s a “point in time” transaction. A great example is selling a physical product; you recognize the revenue when the customer receives the item. If the value is delivered continuously, it’s an “over time” transaction. This applies to things like a year-long software subscription or a consulting project, where you would recognize a portion of the revenue each month as you provide the service.

Can I manage ASC 606 compliance with just spreadsheets? While it might be tempting to use spreadsheets, especially when you're starting out, it's a risky approach that doesn't scale. The standard requires detailed tracking, estimates, and allocations that are incredibly difficult to manage manually without introducing errors. As your business grows and your contracts become more complex, a spreadsheet will quickly become a liability. An automated system is the best way to ensure accuracy, create a clear audit trail, and save your team from countless hours of manual work.

What's the most common mistake you see companies make when implementing this standard? The biggest hurdle for many companies is incorrectly identifying their performance obligations. It’s easy to look at a contract with bundled goods and services and treat it as one single sale. However, ASC 606 requires you to unbundle those items and recognize revenue for each one as it's delivered. Forgetting to separate a software license from its related support services, for example, can throw off the timing of your revenue and lead to inaccurate financial reports.

This feels overwhelming. What's the very first step I should take? The best place to start is with a simple review. Grab a few of your most common customer contracts and walk them through the five-step model described in this post. This exercise will quickly show you where your current process aligns with the standard and where the gaps are. It helps make the abstract rules feel more concrete and gives you a clear idea of which areas—like variable pricing or bundled services—will require the most attention.

Former Root, EVP of Finance/Data at multiple FinTech startups

Jason Kyle Berwanger is an accomplished two-time entrepreneur, polyglot in finance, data & tech with 15 years of expertise. Builder, practitioner, leader—pioneering multiple ERP implementations and data solutions. Catalyst behind a 6% gross margin improvement with a sub-90-day IPO at Root insurance, powered by his vision & platform. Having held virtually every role from accountant to finance systems to finance exec, he brings a rare and noteworthy perspective in rethinking the finance tooling landscape.

Meet with an expert in revenue recognition and order-to-cash accounting and automate revenue close.

Talk with an accountant →*Or watch 2 minute demo here.

Power your high-volume business's revenue compliance and reporting needs with one platform.