Sign in

Request a demo

Talk with an accountant.

Connect with us:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Revenue recognition remains one of the top three causes of financial restatements, even a decade after ASC 606 became standard. For product-led growth (PLG) companies selling through Stripe, app stores, or custom data warehouses, the challenge has intensified dramatically. Adapted from a webinar hosted by Cody Leach, CPA.

.jpg)

The shift to ASC 606 fundamentally changed how companies recognize revenue. Instead of relying on invoices and collectibility, accounting teams now must navigate performance obligations, contract modifications, and variable consideration. More critically, they need access to contract data that lives in systems built for sales teams, not accountants.

This creates a dangerous gap. Tools like Salesforce and HubSpot were never designed with accounting periods in mind, yet they hold the contract information required for proper revenue recognition. Meanwhile, traditional billing systems lack the contract concepts necessary for ASC 606 compliance.

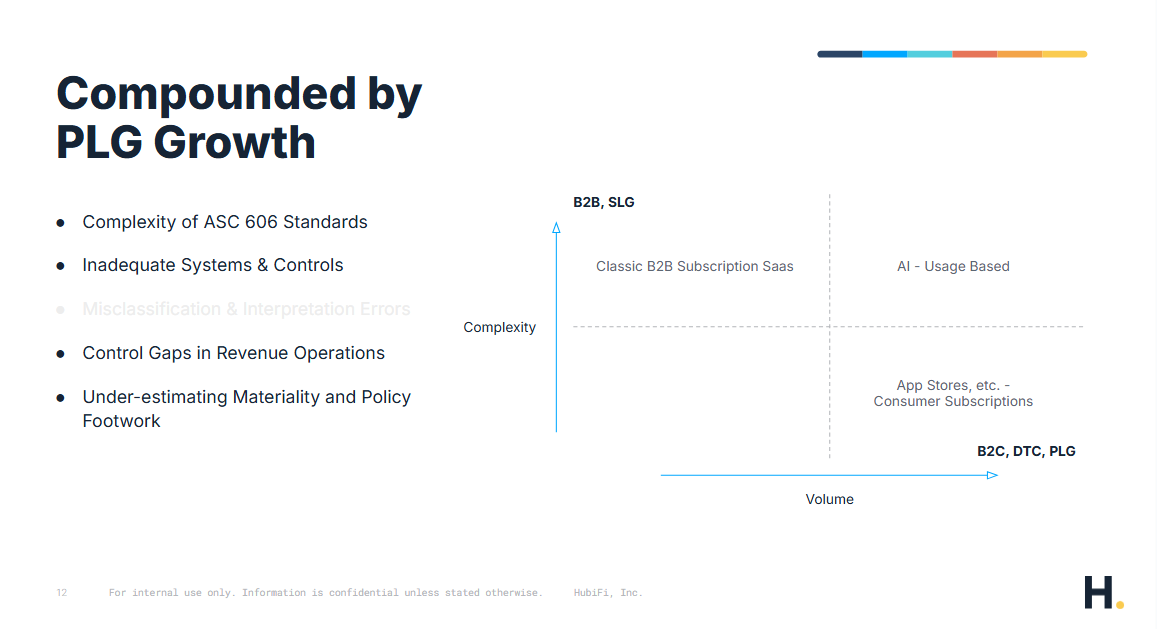

For PLG companies, this problem compounds exponentially. A traditional B2B SaaS company might handle hundreds of contracts annually. A PLG company processes hundreds of thousands of credit card transactions through Stripe, each representing a separate contract requiring proper accounting treatment.

Fast-growing AI companies face a perfect storm of complexity. Companies like Cursor and Perplexity often hire their first accountant three years into hypergrowth, inheriting millions of improperly recorded subscriptions. These companies must somehow restate historical financials while managing:

The tools these companies rely on create their own obstacles. Stripe lacks comprehensive invoice reporting, making it impossible to properly track unpaid invoices that represent actual revenue (and eventual bad debt). Apple provides only two reports to finance teams, neither with sufficient granularity for ASC 606 compliance. Custom data warehouses present the worst scenario: constantly changing data that may not even exist when you need to restate historical periods.

The most frequent mistakes we see:

Customer balance mismanagement: Stripe allows issuing customer credits without providing reporting to track this liability. Companies often discover millions in unrecorded liabilities.

Revenue recognition based on paid invoices: Without proper invoice reporting, companies record revenue only when invoices are paid, missing unbilled revenue entirely.

Proration logic errors: Stripe's subscription and invoicing nuances require careful handling that manual processes simply cannot scale.

Variable consideration complexity: Determining whether refunds constitute variable consideration across millions of transactions proves nearly impossible manually.

ASC 250 governs the restatement process, which follows a specific decision tree. First, determine whether you truly have an error under GAAP or simply a change in accounting principle. If it qualifies as an error, assess materiality using SAB 99 guidance.

Material errors require one of three approaches:

Out-of-period adjustment: The simplest option when the error is small enough to record in the current period without causing material misstatement.

Revision restatement (little "r"): Used when there is a material error in the current year but the error was not material to prior years. You recast current year financials without reissuing historical statements.

Reissuance restatement (big "R"): Required when prior period financials were materially misstated. This triggers full reissuance of historical financials and, for public companies, filing an 8-K.

Once you determine the approach, the technical work begins:

For PLG companies, step two presents the biggest challenge. Recomputing revenue for hundreds of thousands of transactions requires data that often does not exist in accessible form. You need complete historical data because a customer credit issued in year one might still impact balances today.

Professional services firms typically charge $100,000+ for restatement work, requiring months of manual effort. For PLG companies, these firms face the same data limitations as internal teams. They cannot access the granular transaction details needed for accurate recalculation.

One customer received a quote of $600,000 to restate their FY2025 financials using traditional methods. Another needed to restate five years of Stripe data to complete an acquisition but could not obtain the necessary reports.

Automation changes the equation entirely. By connecting directly to contract, billing, and payment systems through APIs, automated solutions can recalculate revenue in days rather than months. The process becomes part of implementation rather than a separate six-figure engagement.

More importantly, automation produces journal entry-level detail rather than summary adjustments supported by Excel spreadsheets. This dramatically reduces audit risk while creating value beyond compliance. The detailed data enables FP&A reporting and disclosure requirements that manual processes cannot support.

Revenue restatements remain a leading compliance challenge, particularly for PLG companies processing high transaction volumes through systems never designed for accounting. The gap between where contract data lives and where accounting happens creates persistent risk. Traditional professional services approaches prove both expensive and inadequate when underlying systems lack proper reporting. Automated solutions can complete restatements in weeks instead of months while producing audit-ready detail that adds operational value beyond pure compliance.

Accounting Automation | Product | Technical Accounting | Accounting Systems Nerd

Cody Leach, CPA is a technology and automation focused CPA helping finance leaders bring their processes into the 21st century. He's advised finance teams around technical accounting and automation - such as Cursor, Meta, Strava, and many others and has helped SaaS and AI finance teams turn messy and usage data into clean, automated revenue reporting that actually matches how the business runs. Former KPMG auditor, Cody holds in Masters in Accounting from North Carolina State University. He is a CPA.

Meet with an expert in revenue recognition and order-to-cash accounting and automate revenue close.

Talk with an accountant →*Or watch 2 minute demo here.

Power your high-volume business's revenue compliance and reporting needs with one platform.